The value of your vehicle starts depreciating as soon as you drive it off the lot, especially for newer cars, and most cars will lose 20% of their value within the first year of leasing. If you get into an accident and total your car, a standard insurance policy will only cover the current market value of your car and not the full amount you owe on your loan. If you’re worried about losing money, you can protect yourself against potential financial losses with gap insurance. Gap insurance (guaranteed auto protection insurance) pays the difference between your vehicle’s value and how much you owe on it. If you owe more money on your financed vehicle than its current market price, then gap insurance is a good option for you. Learn what gap insurance does (and doesn’t) cover below.

Key Takeaways:

- Protect Your Investment: Gap insurance covers the difference between your car’s depreciated value and the amount you owe on your loan, safeguarding you from financial loss if your vehicle is totaled or stolen.

- Who Needs It?: Gap insurance is ideal for those who owe more on their car than its current market value, especially if you made a small down payment, have a long lease, drive long distances, or purchased a high-value vehicle.

- Affordable Coverage: Gap insurance is typically affordable and can be purchased from your auto insurance provider, often at a lower cost than through a dealership or finance company.

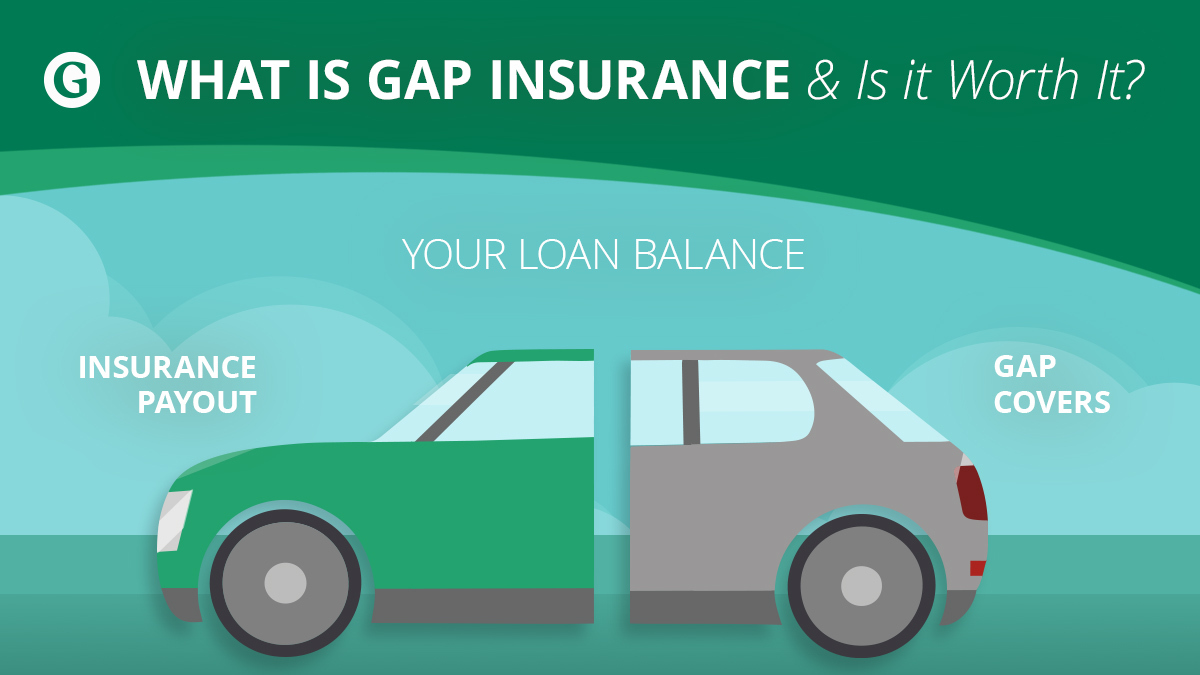

What Does Gap Insurance Cover?

Gap insurance, typically available on cars less than 5 years old, helps to pay the difference between the depreciated value of your vehicle and what you still owe on your car, subject to policy limits. Gap insurance covers your totaled car when it’s no longer usable. If you’re in an accident and your financed car is damaged beyond repair, gap insurance will cover the cost of what you owe. Gap insurance will also cover the cost of your vehicle if it’s stolen.

Gap insurance only covers your car when it can’t be fixed. Therefore, gap insurance won’t cover you if your car gets in an accident and is still salvageable. Gap insurance only covers expenses related to your vehicle, so it doesn’t cover things like bodily injury and death. Lastly, gap insurance won’t cover your comprehensive or collision deductible.

Common Myths About Gap Insurance

There are several misconceptions about gap insurance. One common myth is that gap insurance covers mechanical breakdowns, which it does not. Another myth is that gap insurance is unnecessary if you have comprehensive and collision coverage. In reality, these coverages do not pay off your loan balance if your car is totaled or stolen.

Is Gap Insurance Worth It?

Only drivers who are financing their vehicles are eligible for gap insurance. Gap insurance can be a worthy investment for drivers who owe more on their car than its current market value. If you want to learn if gap insurance is a good fit for you, simply approximate your car’s current value and subtract it from what you owe on your car. You can learn your car’s value online via sites like Kelly Blue Book or by visiting your local appraiser. In addition to calculating “the gap,” you might be a good fit for gap insurance if any of these situations apply to you:

- Your lease or loan provider requires it. Your financing company may require gap insurance to protect them from financial loss.

- You made less than a 20% down payment or selected a long lease. A smaller down payment or a lengthy lease means that your loan balance is decreasing slowly, so your vehicle may be depreciating faster than you can pay it off. This is especially true during the first few years of your lease.

- You purchased a luxury or high-value car. These types of vehicles depreciate faster than the average car, so your loan amount will probably be greater than your car’s value.

- You rolled over negative equity from an old car loan into your new loan.

- You drive your car long distances. Adding a lot of mileage to your car will cause it to depreciate faster.

The Cost of Gap Insurance

Gap insurance is typically affordable, but costs can vary based on several factors, including the vehicle’s make and model, your location, and your insurance provider. On average, you might pay between $20 and $40 per year if you add it to your existing auto insurance policy. It’s important to compare rates from different providers to find the best deal.

Where Can I Get Gap Insurance?

Your dealership on finance company may offer gap insurance on their vehicles, but it’s typically cheaper to purchase gap insurance from your auto insurance company.

If you’re looking for affordable coverage, The General has a range of policies that fit every budget and driving record, and we offer gap insurance in some states! If you have questions about your coverage, you can check your coverage online, contact us directly, schedule a call, or chat with one of our customer service agents. Read some of our five-star reviews and see how we put our customers first or learn more about car insurance on our blog.